A 300-life employer accepting 8.5% annual medical trend without strategic intervention overspends by nearly $4 million over five years compared to an actively managed self-funded plan. Here's the math carriers hope you never run.

A fully-insured to self-funded transition takes 12 months done right. Here's the phase-by-phase roadmap, from actuarial analysis through employee communication and go-live.

When fully-insured claims run light, the carrier keeps the surplus and hands you a renewal increase. Here's how self-funding puts that money back in your plan.

When employees don't understand their health plan, they make worse decisions that undermine the actuarial assumptions behind your plan design. That's not an HR communication gap. It's a direct hit to your plan budget.

HR professionals are absorbing blame for a healthcare cost crisis driven by specialty drugs, catastrophic claims, and PBM complexity they don't control. Here's how to reframe the problem before the next renewal cycle.

Employees see their payroll deduction and think that's the cost of insurance. They have no idea you're covering $1,400 or more per month on top of that. That gap is why benefits fail as a retention tool.

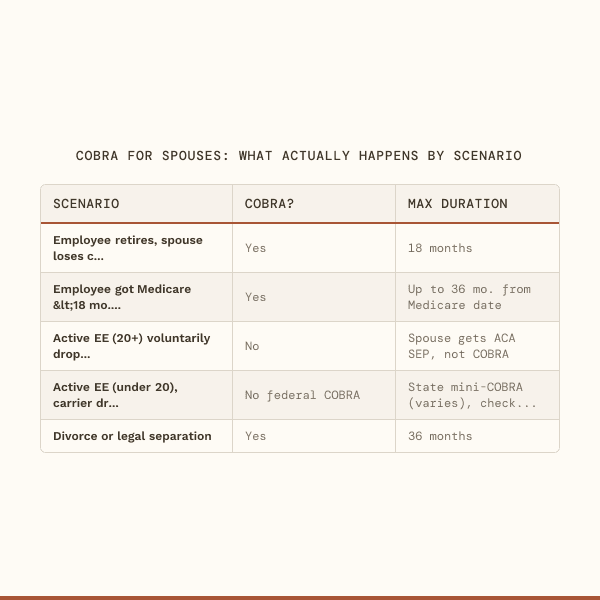

HR teams hear "Medicare" and assume the spouse gets 36 months of COBRA. The real answer depends on when Medicare started, when employment ended, and whether coverage was actually lost. Here's what the rules actually say.

Level-funded plans are sold as self-funding but they're not. The carrier controls your stop-loss, your vendors, and potentially your surplus. Here's what the structure actually looks like.

The PCORI fee jumped to $3.84 per covered life for plan years ending in the 2025-2026 window. Here's a step-by-step guide to calculating covered lives and filing IRS Form 720 before the July 31, 2026 deadline.