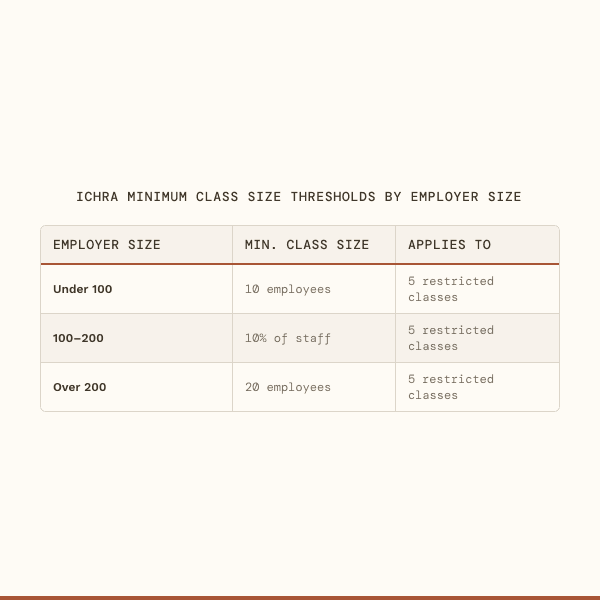

There are 11 legal ICHRA employee classes, but split designs that mix a group plan with an ICHRA trigger minimum class size rules for five of them. Here's how the thresholds work and where most employers get it wrong.

DIR fees grew 107,400% in a decade and peaked at $9.5 billion. CMS reformed them out of Medicare. Your employer plan still has them. Here's where the money goes and what to do before the CAA catches up in 2029.

The No Surprises Act left real gaps. Ground ambulance, PE-backed firms gaming IDR at 920% of market rates, and $5 billion in system costs since 2022. Here's where self-funded employees are still exposed and what to do about it.

Your TPA handles administration, but ERISA fiduciary liability stays with you. With 155 ERISA lawsuits in 2025 and new CAA disclosure mandates, here's what to check in your ASA before renewal.

The Transparency in Coverage rules require your health plan to post three machine-readable files every month. Most employers have no idea whether their vendor is actually doing it.

Self-funded employers owe a PCORI fee by July 31 each year, filed on IRS Form 720. The 2026 rate is $3.84 per covered life for calendar-year plans, and first-timers rarely see it coming.

Illinois SB3114, the Transparency in Downcoding Act, passed 59-0 and 111-0 and awaits the Governor's signature. Self-funded ERISA plans are exempt, but the law exposes a claims practice every employer should be auditing.

The CAA requires brokers to disclose all compensation before your renewal is signed. Most employers never ask for it, and that creates real fiduciary exposure.

Form 5500 is due July 31 for December 31 plan years. Here's the 60-day checklist self-funded employers need to gather Schedule H, C, and A data and coordinate with their TPA before the deadline.

The DOL flags Form 5500 filings using predictable patterns, including missing audits, late contributions, and missing participants. Here's what they're looking for in 2026.

Your broker may be earning indirect compensation from the carrier recommending your plan. Here are the specific red flags, compensation structures, and service failures that signal it's time to make a change.

The IRS penalty for a late Form 5500 is $250 per day, capped at $150,000. The DOL adds up to $2,529 per day with no cap. Here's what to do before July 31.